Apartments

Apartments Villas

Villas Townhouses

Townhouses Penthouses

Penthouses Commercial

Commercial See All Properties

See All PropertiesSignature Collection

Explore Signature Commercial

Commercial Property Management

Property Management List Your Property

List Your Property Mortgages

Mortgages Conveyancing

Conveyancing Short Term Rentals

Short Term Rentals Property Snagging

Property Snagging Partner Program

Partner Program Currency Exchange

Currency Exchange PRYPCO

PRYPCO Ethnovate

Ethnovate Plots

Plots

Dubai’s real estate market closed the month with activity remaining strong across both off-plan and secondary segments. Stay ahead of Dubai’s fast-moving property sector with the Provident Dubai Real Estate Market Report for April 2026, whether you are an investor, buyer, developer, or industry professional.

From insights into off plan properties in Dubai to changing buyer behavior and luxury market performance, this report explores the key performance indicators, growth areas, and emerging opportunities shaping the market today.

Key Takeaways

Here is the summary of the Dubai real estate market for April 2026:

- Dubai recorded 14,076 property transactions worth AED 48.4 billion

- Average property prices reached AED 1,840 per sq. ft.

- Off-plan sales contributed AED 35.8 billion, showing continued investor confidence in future developments

- Villas recorded the strongest annual price growth, increasing by 42.6% compared to 2025

- Cash buyers made up a larger share of transactions, signaling stronger market confidence and higher equity participation

- Luxury waterfront communities and master-planned developments remained among the top-performing investment destinations

- Commercial real estate activity also increased, with AED 3.7 billion in off-plan commercial transactions

What are the key trends in Dubai property market April 2026?

The latest Dubai real estate insights for April 2026 show a market gaining ground on three fronts at once: more deals, increased transaction values, and a higher proportion of equity-funded transactions.

| Market Metric | April 2026 |

| Total Sales Volume | 14,076 Transactions |

| Total Sales Value | AED 48.4 Billion |

| Average Price per sq. ft. | AED 1,840 |

Including DLD direct sale transactions. Excludes mortgage registrations and gift transfers.

The total sales value growing faster than transaction volume shows buyers are moving toward higher-priced properties and larger investments. The AED 1,840 average price per sq. ft. also reflects continued upward pricing pressure across premium communities and waterfront developments.

Communities such as Dubai Hills Estate, Palm Jumeirah, and Dubai Creek Harbour continued attracting both local and international investors during the month.

How Dubai’s Off-Plan Market Performed in April 2026

Off-plan activity continued to set the pace for the broader market. New launches across master-planned communities in Dubai pulled steady demand from both investors and end-users.

| Off-Plan Metric | April 2026 |

| Total Sales Volume | 10,563 Transactions |

| Total Sales Value | AED 35.8 Billion |

| Average Price per sq. ft. | AED 1,920 |

The off plan properties in Dubai accounted for nearly three-quarters of Dubai’s total market value in April. This shows how strongly buyers continue favoring newly launched projects, flexible payment plans, and future-focused communities.

The higher average price per sq. ft. compared to the broader market also indicates that investors are increasingly purchasing premium off-plan inventory in areas such as Dubai Islands, Dubai South, and Palm Jebel Ali.

Average Sale Prices

| Property Type | Average Price | Vs 2025 |

| Apartment | AED 1.5M | +18.8% |

| Villa | AED 5M | +42.6% |

| Plot | AED 4.2M | -5.7% |

Villa prices recorded the strongest annual growth, rising 42.6% year-on-year. This reflects ongoing demand for larger homes and luxury family communities, especially in areas like Dubai Hills Estate, Tilal Al Ghaf, and Palm Jebel Ali.

Apartment values also continued climbing steadily due to investor demand for rental income and branded residences.

The slight decline in plot prices may indicate more strategic long-term land acquisitions rather than speculative trading activity.

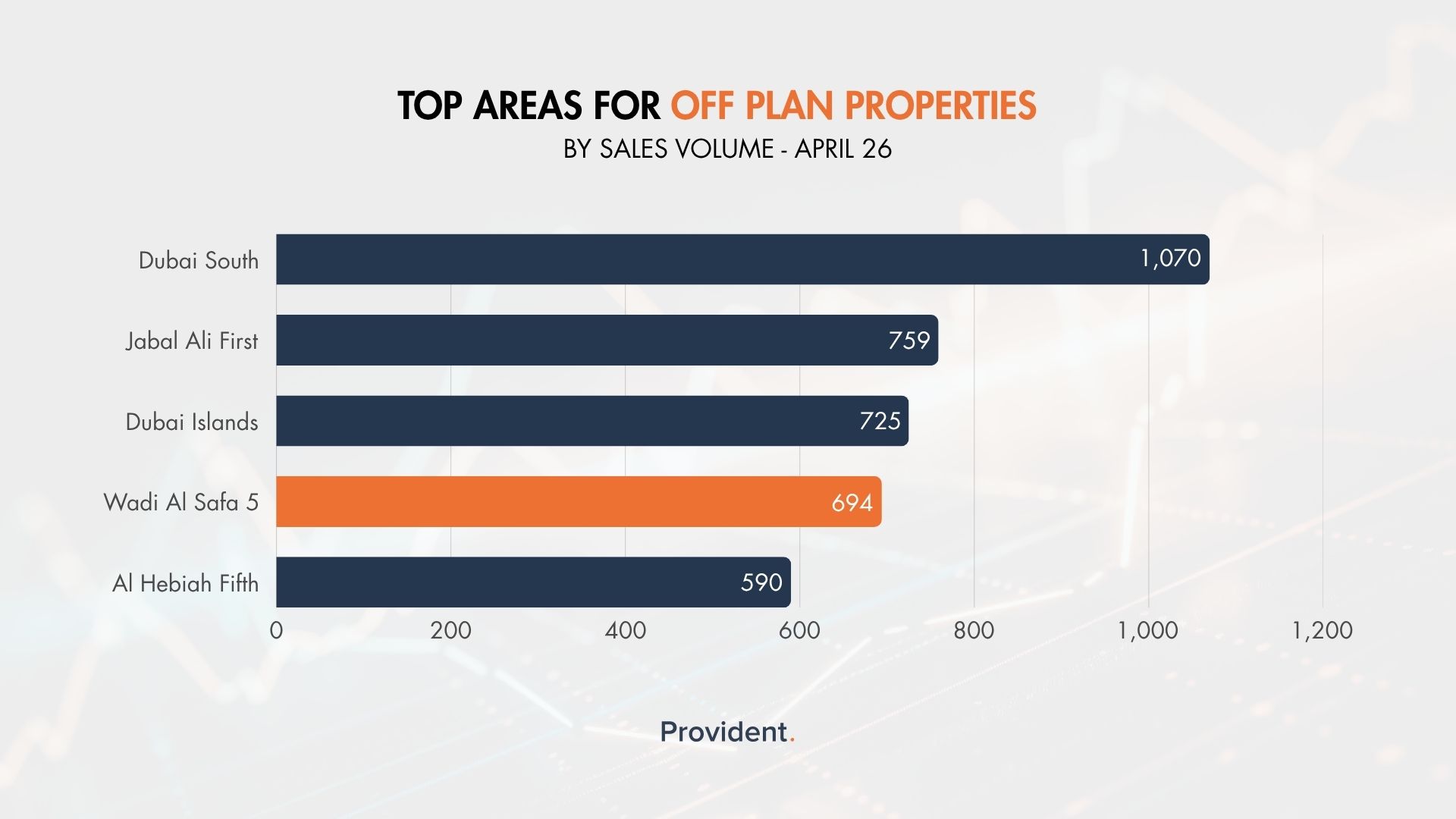

Top Off-Plan Areas by Transaction Volume

Dubai South led transaction activity due to growing demand around Al Maktoum International Airport, Expo City, and future infrastructure expansion. Despite having fewer transactions than Dubai South, Dubai Islands generated significantly higher value, indicating stronger luxury and waterfront positioning.

Jabal Ali First and Al Hebiah Fifth also continued benefiting from large-scale master-planned developments and strong investor activity.

For investors researching emerging growth corridors, explore:

Off-Plan Commercial Performance in April 2026

| Commercial Metric | April 2026 |

| Sales Volume | 450 Transactions |

| Sales Value | AED 3.7 Billion |

Commercial off-plan activity scaled up in April, with average transaction values totaling approximately AED 8.2M.

This level of commercial investment usually comes from institutional buyers, business owners, and investors targeting long-term rental income from office and retail assets.

The increase in commercial demand also aligns with Dubai’s broader economic expansion and rising office occupancy rates.

Expo City Branded Residences

Expo City’s Luxury Homes

Discover innovative living in this iconic destination with Provident. Claim your spot today!

How Dubai’s Secondary Market Performed in April 2026

The secondary market recorded growth in both transactions and value, continuing to serve buyers seeking ready inventory. Activity in this segment is smaller in scale than off-plan, but offers immediate occupancy and proven rental performance.

| Secondary Market Metric | April 2026 |

| Total Sales Volume | 3,414 Transactions |

| Total Sales Value | AED 12.2 Billion |

| Average Price per sq. ft. | AED 1,550 |

The secondary market’s lower average price per sq. ft. compared to off-plan reflects stronger activity in established communities and ready properties.

This segment remains particularly attractive to end-users and rental investors looking for completed assets with immediate income generation potential.

Popular ready communities included:

Average Sale Prices

| Property Type | Average Price | Vs 2025 |

| Apartment | AED 1.3M | +1.2% |

| Villa | AED 3.9M | +12.8% |

| Plot | AED 13.5M | -117.6% |

Secondary villas continued outperforming apartments, showing sustained demand for ready family homes in mature residential communities.

The sharp movement in plot pricing reflects fluctuations caused by a smaller number of ultra-high-value land transactions rather than broad market weakness.

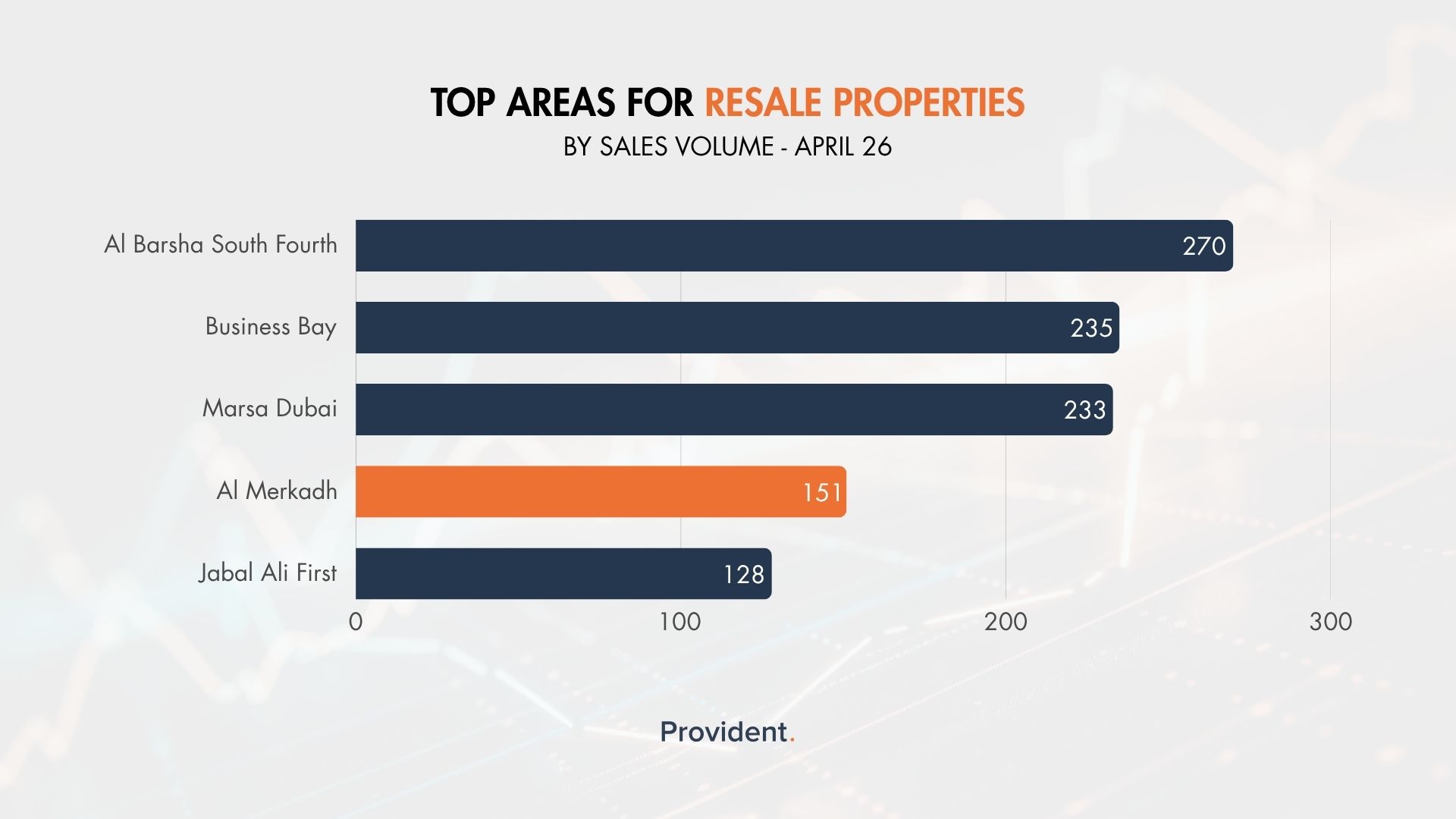

Top Areas for Resale (Ready Properties)

Al Barsha South Fourth continued attracting families looking for larger homes near schools and established infrastructure.

Business Bay and Marsa Dubai also remained highly active because of their strong rental demand, central locations, and appeal to investors seeking short-term rental income.

Dubai Rental Market Trends in April 2026

The rental market in April 2026 showed stable residential rents and strong growth in commercial leasing demand.

| Rental Segment | Average Annual Rent |

| Apartment | AED 70,000 |

| Villa | AED 175,000 |

| Commercial | AED 81,000 |

Apartment rents remained relatively stable, suggesting the market may be entering a healthier balancing phase after several years of aggressive rental growth.

Villa rents recorded a slight correction month-on-month, but demand for larger homes remained strong overall.

The sharp rise in commercial rents reflects increasing business activity and limited prime office supply across Dubai’s key commercial districts.

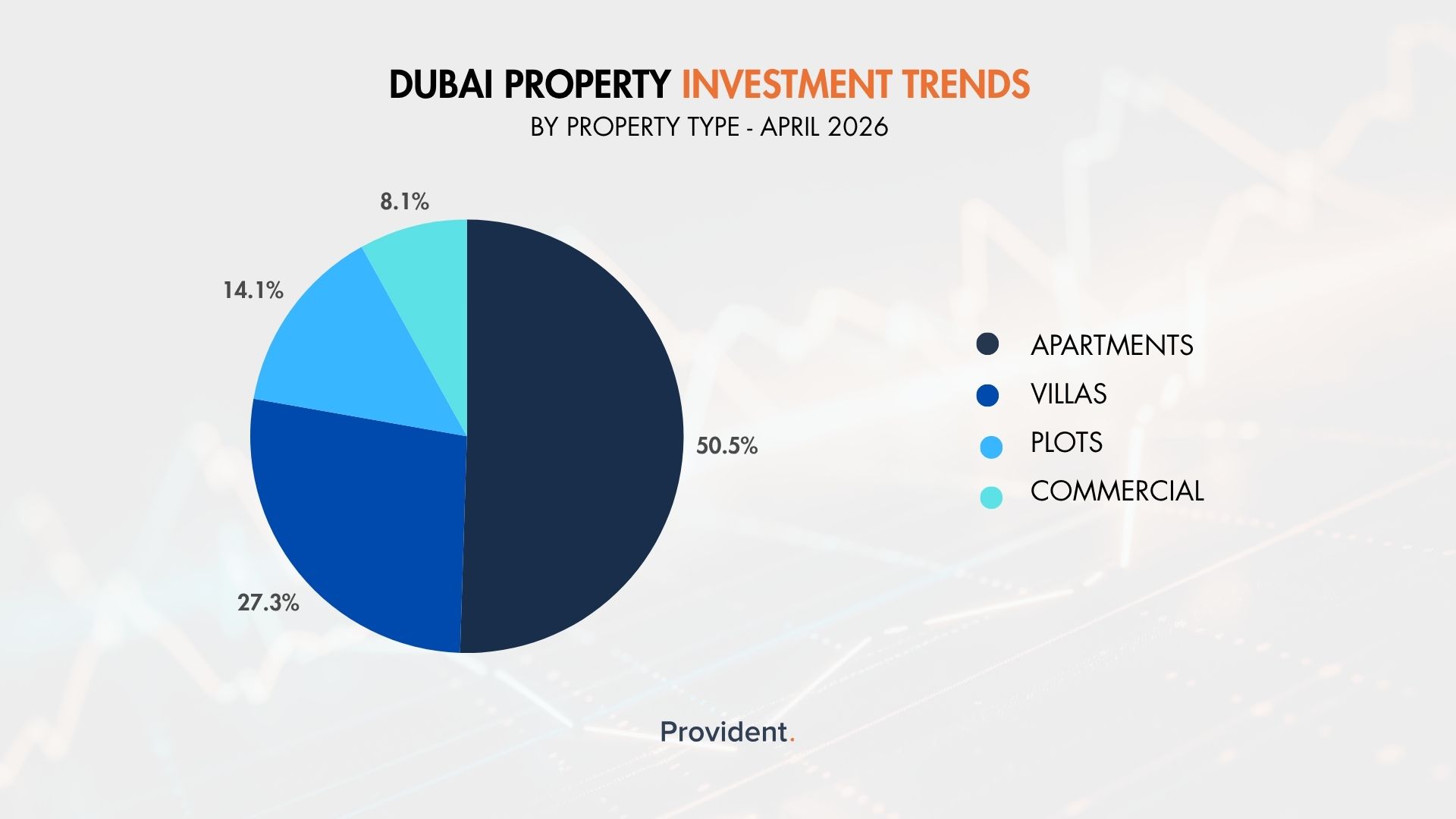

Dubai Property Investment Trends by Property Type

April’s capital allocation stayed weighted toward residential, with apartments and villas absorbing more than three-quarters of total value.

Apartments continuing to absorb half of the market value shows that investor demand remains heavily focused on rental-producing residential assets.

The 27% allocation toward villas highlights continued demand from high-net-worth buyers and families relocating to Dubai.

The 14% share allocated toward plots is especially important because land purchases typically come from developers, institutional investors, and family offices preparing for future supply cycles.

Dubai Luxury Property Market in April 2026

The luxury segment held steady in April, recording several transactions above AED 60 million across both apartments and villas.

| Project | Sale Price |

| Aman Residences Tower 2 at Jumeirah Second | AED 171M |

| Baccarat Residence T1 at Downtown Dubai | AED 122M |

| Building C at Marsa Dubai | AED 118M |

| Aman Residences Tower 1 at Jumeirah Second | AED 70M |

| Orla Infinity By Omniyat at Palm Jumeirah | AED 65M |

These numbers show continued global demand for ultra-prime branded residences in Dubai.

The significant pricing gap between Aman Tower 2 and the lower-ranked transactions demonstrates how rarity, branding, and waterfront positioning continue driving luxury pricing beyond traditional market averages.

| Project | Sale Price |

| Eden Hills | AED 76M |

| Al Barari | AED 75M |

| Emerald Hills at Dubai Hills | AED 75M |

| Sobha Estates | AED 65M |

| Signature Villas | AED 61M |

Meanwhile, luxury villa pricing remained tightly grouped between AED 61M and AED 76M, showing that land value and location fundamentals continue anchoring the ultra-luxury villa market.

Communities such as Dubai Hills Estate, Al Barari, and Palm Jumeirah remain among Dubai’s strongest-performing luxury residential destinations.

Expert Insight

Provident's Dubai Real Estate Market Report For April 2026 reflects a market that is still expanding, but in a more structured and capital-driven way than previous growth cycles.

One of the clearest indicators this month was the continued dominance of the off-plan segment. With 76% of total transaction volume coming from off-plan sales, investors are clearly positioning themselves around future infrastructure, master-planned communities, and long-term appreciation opportunities.

Areas such as Dubai South, Dubai Islands, and Jabal Ali First continue benefiting from this trend as buyers move toward emerging growth corridors.

The commercial segment also showed meaningful momentum during April 2026. Rising office rents and stronger commercial transaction values suggest that Dubai’s business environment continues expanding alongside population growth and foreign investment inflows.

Overall, the April 2026 market data suggests Dubai is transitioning from a rapid post-pandemic growth cycle into a more mature expansion phase defined by:

- Higher-quality investment activity

- Long-term capital positioning

- Strong off-plan absorption

- Infrastructure-led demand

- Continued international investor confidence

- Increasing focus on premium and lifestyle-driven communities

Sources: The data in Provident Dubai Real Estate Market Report for April 2026 is sourced from Dubai Land Department (DLD), DXB Interact, Property Monitor, and Provident’s transaction database.

FAQs

Yes. Dubai’s real estate market continues showing growth across transaction value, pricing, and investor participation. April 2026 recorded AED 48.4 billion in property sales alongside rising average prices per sq. ft., reflecting continued market expansion.

Dubai South, Dubai Islands, Business Bay, Dubai Hills Estate, Palm Jumeirah, and Jabal Ali First remain among the strongest-performing areas due to infrastructure expansion, waterfront developments, and growing investor demand.

Property prices continue rising across many premium communities, especially within villas, waterfront developments, and branded residences. However, growth has become more selective depending on location, supply, and asset quality.

Higher land acquisition activity usually indicates developers and institutional investors are preparing for future project launches and long-term population growth. Plot purchases are often an early indicator of future development cycles.

For more information, get in touch with us at Provident